The Deafening Silence on Social Security’s Looming Insolvency

Social Security will become insolvent in just 16 years. Who says so? The people who run the Social Security Administration.

James R. Harrigan Antony Davies July 3, 2019

As the 2020 presidential campaign heats up, it’s disturbing that members of both parties seem unwilling to talk about Social Security. It appears that the program is on such shaky ground that even its mention is political dynamite. How bad is it? Social Security will become insolvent in just 16 years. Who says so? The people who run the Social Security Administration.

Social Security Will Be Bankrupt

Let’s be crystal clear about what’s happening. Politicians and bureaucrats used to use the word “insolvent” to describe Social Security’s future. They’ve now started to use the term “reserve depletion.” The rest of us should use the correct term: bankrupt. Social Security will be bankrupt in 16 years. Politicians pull a sleight of hand by saying (when they manage to say anything at all) that Social Security won’t be bankrupt because it can continue to make 80 percent of promised payments into the infinite future. Everywhere outside the Washington beltway, “bankrupt” means the inability to make promised payments. Being able to make partial payments doesn’t count. Those in doubt are welcome to try the argument with their credit card companies.

The bottom line is that within 16 years, either Social Security recipients will have to take a 20 percent benefits cut, or workers will have to incur a 20 percent payroll tax increase. Either way, at least someone, and likely everyone, is going to be getting a far worse deal from Social Security than Social Security has promised.

That alone should be enough to give reasonable people pause. But, even if some last-minute miracle pulls Social Security back from the financial brink, a number of serious problems will remain. It turns out that Social Security is more of a class system than politicians would like to admit, and it puts some of us at a material disadvantage to others in ways no politician would want to discuss. But first, some basics.

First, people often take issue with the fact that the Social Security tax is capped. In 2019, each worker pays Social Security tax on the first $133,000 in wages earned during the year. But wages a worker earns beyond the $133,000 are not subject to the Social Security tax. At first glance, this appears unfair. Except Social Security benefits are also capped. When people with wages exceeding $133,000 retire, they only receive Social Security benefits on the first $133,000 of income they earned. Social Security benefits and Social Security taxes are capped at the same amount.

What politicians who talk about “raising the cap” on Social Security really want is to raise the cap on Social Security taxes while keeping in place the cap on benefits. That change would significantly alter the nature of Social Security from a program intended to redistribute income from workers to retirees to a program intended to redistribute income from the rich to the poor. And this will have at least one very undesirable unintended consequence.

The Tax Cap Hurts Entrepreneurs

The Social Security tax cap is a boon to budding entrepreneurs. Around 45 million Americans have “side businesses.” These are starter businesses—hobbies that have started to generate income or gig arrangements (like driving for Uber or renting out property on Airbnb) that generate a little extra spending money. Many of these side businesses remain simply that. But over time, some become full-fledged businesses that provide the owners’ main sources of income and possibly even employ others.

It turns out that the Social Security tax cap gives an unintended, though welcome, incentive to grow these side businesses. A couple who have regular jobs earning $70,000 total, and who can grow a side business to the point of generating an additional $63,000, can break through the Social Security tax cap. Any income their side business generates beyond $63,000 is exempt from the Social Security tax.

That’s a 12.4 percent boost on that extra income and is a strong incentive to keep growing the side business. But, raising the Social Security tax cap slaps a 12 percent tax on side businesses like this that are on the verge of becoming full-fledged businesses. If a malicious politician were to design a tax code to dissuade people from starting businesses and creating jobs, it would look a lot like an increase in the Social Security tax cap.

Social Security Can’t Be Passed Down

Second, there is an effective 100 percent death tax on Social Security benefits. As with a savings account, a house, or any other asset, a person can leave his private retirement account to heirs. Not so with Social Security benefits. When the recipient dies, most of his remaining benefits cannot be left to heirs. Spouses can continue to receive some benefits, but only if the spouse earned less than the recipient. The recipient’s children can receive some benefits, but only while they are minors. Apart from these exceptions, unused Social Security benefits revert to the federal government upon the recipient’s death. The 100 percent death tax dramatically reduces the value of Social Security benefits. And this stacks the deck against blacks, males, and particularly black males.

Over the course of his working life, the median white male can expect to pay around $250,000 in Social Security taxes and to receive $280,000 in benefits (adjusted for the probabilities of unemployment and mortality). The $280,000 in benefits represents a return of one-third of 1 percent above inflation on the $250,000 in taxes. While the median white male does not get anything approaching a good return on his Social Security taxes, he at least breaks even over time. The median white female does a fair bit better than her male counterpart. Because the median female earns less than the median male, she can expect to pay less in Social Security taxes—around $210,000. But because she can expect to live longer, she can expect to receive more benefits—around $360,000. That’s a return of 1.5 percent above inflation.

A black male who earns the same as the median white male can expect a return of one-third of one percent below inflation. The median black male doesn’t break even because of the combination of a shorter life expectancy and the 100 percent Social Security death tax. Similarly, the median black female can expect a return of 1.2 percent above inflation.

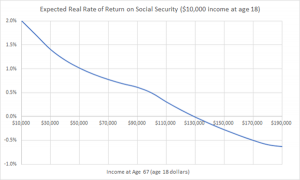

Differences in mortality due to race and gender affect the return on Social Security taxes, but the return is mostly influenced by the person’s earnings history. And here, we see that Social Security, as an investment, ends up being a worse deal for higher-income earners. The chart below shows the expected real return for a worker who earns $10,000 at age 18 and whose income rises to the level shown on the horizontal axis by age 67 (all figures are adjusted for inflation). For example, a worker who earns $10,000 at age 18 and continues to earn $10,000 per year (adjusted for inflation) every year until age 67 can expect to receive Social Security benefits that are the equivalent of a 2 percent return above inflation on the Social Security taxes the worker paid. A worker who earns $10,000 at age 18 and whose annual income rises steadily to $170,000 (adjusted for inflation) by age 67 can expect to receive Social Security benefits that are the equivalent of one-half of 1 percent below inflation on the taxes the worker paid.

Source: Figures are constructed according to the AIME and PIA formulas from the Social Security Administration.

As an investment, Social Security is a breakeven proposition for the worker who starts at an annual wage of $10,000 at age 18 and rises to $130,000 by age 67—that is, a worker who averages $70,000 per year over the course of a career. Workers who earn less than an average of $70,000 per year over their careers end up receiving back (adjusted for inflation) more money than they paid in. Workers who average more than $70,000 per year end up paying in more than they receive back.

But for all workers, the possible returns on Social Security taxes range between a low of about two percent less than inflation to a high of two percent more than inflation. That’s the worst and the best a worker can expect from Social Security. And that raises an important question: how do the returns on Social Security taxes compare to the returns on private investments?

Social Security Is Not a Safe Investment

S&P 500 stocks have returned an average of 6.6 percent above inflation over the past 30 years. Triple-A corporate bonds have returned 3.6 percent above inflation. Social Security defenders are quick to point out that stocks and bonds are subject to market risks—they might return zero, or even something negative. That’s true, but the implication that Social Security is a safe investment is false. Remember that Social Security is, by its own admission, within 16 years of bankruptcy. Further, the Supreme Court has ruled (Flemming v. Nestor, 1960) that Social Security benefits are not a contractual right. Workers are obligated to pay Social Security taxes, but the government is not obligated to pay Social Security benefits.

Social Security is supposedly “safe” because it invests the payroll taxes it collects in US Treasury bonds, and US Treasury bonds are backed by the US government. Putting aside for the moment the increasing likelihood that the federal government itself is on the brink of insolvency, one could attain the same supposed safety of Social Security by investing privately in US Treasury bonds.

In fact, such an investment would be safer than Social Security because it would not be subject to Social Security’s 100 percent death tax, and US Treasury bills are a contractual obligation—the government would be legally obligated to give you back your money. Further, over the past 30 years, the real return on 10-year Treasury bonds has been 2.2 percent above inflation. Investing privately in US Treasury bonds yields a greater return and less risk than Social Security.

Is Social Security Worth Saving?

This raises a critical question: Why are we trying to save Social Security at all?

There is literally no reason—at least not for taxpayers. Taxpayers would get a much better deal, both in terms of risk and return, if they kept their Social Security taxes and invested them privately. And, we could eliminate a massive government bureaucracy that accounts for one-quarter of the entire federal budget. Social Security does provide a safety net for the poorest retirees and those who are unable to work. That function of Social Security is worth retaining. But that function is a very small part of what Social Security does.

Social Security as it is presently construed will blow up in our faces, and that will happen relatively soon. The longer politicians wait to address the problem, or the longer they can put off the reckoning through stop-gap measures, the bigger the boom will be. If there is a solution, it lies in shutting Social Security down. That no politician will even mention the problem speaks to the coldest of all political realities: Washington would rather retain a failing program if fixing the program means losing control of it. Why? Because political leaders are motivated by power every bit as much as business leaders are motivated by profit. And retaining power means maintaining control, no matter the cost to working Americans.

That we are in an election cycle and none of the 23 candidates for the presidency is talking about this should have everyone’s attention. The silence is deafening.

James R. Harrigan is Managing Director of the Center for Philosophy of Freedom at the University of Arizona, and the F.A. Hayek Distinguished Fellow at the Foundation for Economic Education. He is also co-host of the Words & Numbers podcast.

Dr. Antony Davies is the Milton Friedman Distinguished Fellow at FEE, associate professor of economics at Duquesne University, and co-host of the podcast, Words & Numbers.

{kind=link}